Weekly Market Update: 04 February 2026

Volatility Returns as Markets Digest Macro Shocks

It was an extremely volatile week across global markets, with risk assets hit by a combination of escalating catalysts, including fresh uncertainty around the incoming Fed Chair, rising geopolitical tensions, and tightening macro conditions. The most notable move came from commodities, where silver suffered a sharp ~40% drawdown, an unusually violent move for what remains one of the largest and most liquid assets in the world.

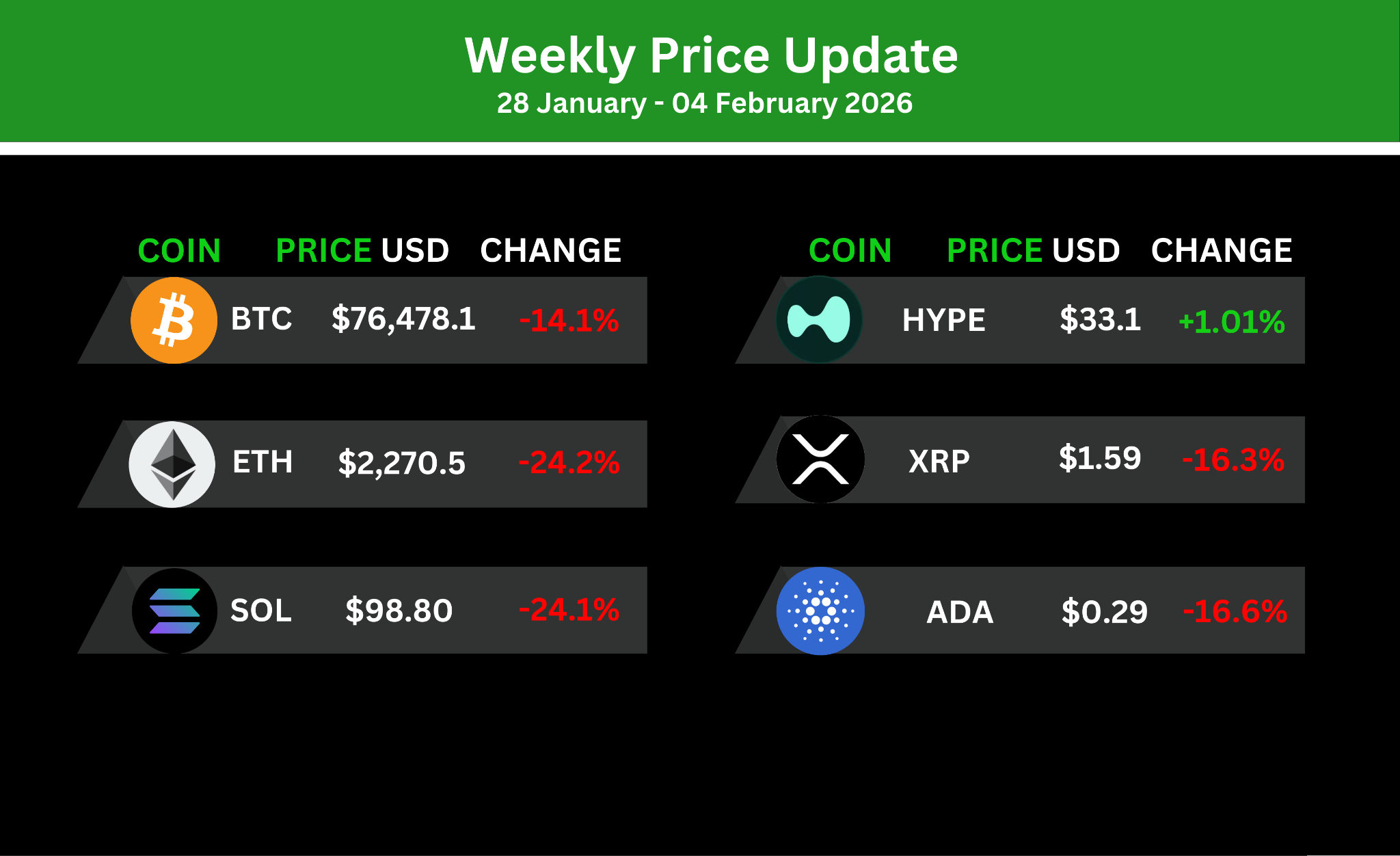

That stress quickly spilled into crypto. Bitcoin recorded its lowest level since November 6, 2024 and finished the week down -14.88%, while Ethereum saw an even deeper drawdown, closing -25%. The speed and magnitude of the move reflected forced deleveraging and capitulation, with volatility rising across both traditional and digital markets.

Warsh Nomination Sparks Metals Shock

On January 30, 2026, President Trump announced Kevin Warsh, a former Federal Reserve governor (2006–2011), as his choice to replace Jerome Powell as Fed chair beginning in May. The announcement acted as the immediate trigger for the metals selloff, functioning more as a sentiment catalyst than a true shift in monetary conditions.

Warsh has historically been viewed as more hawkish on inflation than Powell, favouring a stronger dollar and tighter policy over aggressive easing. That framing provided institutions and systematic flows with a clean narrative justification to reduce exposure to gold and silver. It also conflicted with the broader Trump policy message, where lower rates would typically weaken the dollar and support precious metals.

Risk appetite fell sharply across markets, with over $400B wiped from the crypto market over the weekend. Reported moves on the day were severe: Silver down ~35–40%, gold down ~15–20%, and Bitcoin down ~8–12%. Still, zooming out, silver remained up over 20% for January, while gold held above $4,800/oz, representing gains of more than 80% since the start of 2025.

One of the most striking features of the crash was the divergence between paper and physical pricing, revealing the leverage embedded in precious metals markets. During the worst of the selloff, silver traded near $92/oz on COMEX while trading closer to $130/oz in Shanghai, a gap of over 40%. In Tokyo, physical silver reportedly reached $150/oz. This wasn’t a pricing error — it suggests the move was driven by paper market deleveraging, while real physical demand remained intact.

A Fed Chair Who Understands Bitcoin

Additionally, despite Warsh’s historical hawkish stance, he has also publicly acknowledged Bitcoin, calling it "the newest, coolest software that will allow us to do things that we have never done before”. Further, when asked directly if Bitcoin makes sense, he states: "Bitcoin does make sense as part of a portfolio in this environment where you have the most fundamental shift in monetary policy since Paul Volcker," and crucially adds: "For anyone under 40, Bitcoin is your new gold." Warsh's pro-Bitcoin stance as Fed chair is bullish because he frames crypto as a legitimate policy tool and market discipline mechanism rather than a threat. By being the first Fed leader in history who actively endorses Bitcoin adoption, it eliminates the regulatory headwind that plagued previous administrations and positioning crypto for mainstream institutional adoption in 2026.

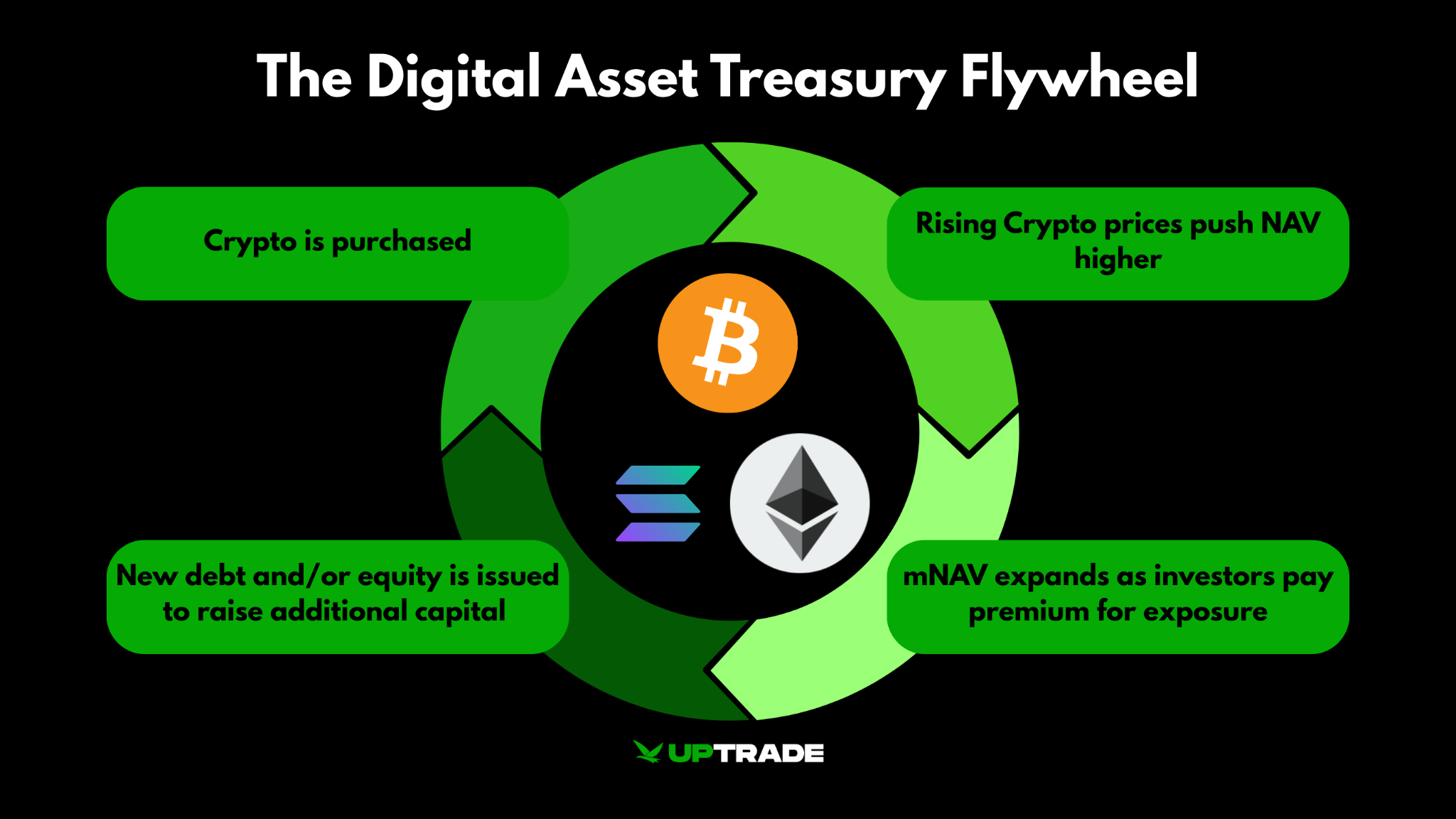

Crypto Treasuries: From Premium to Discount

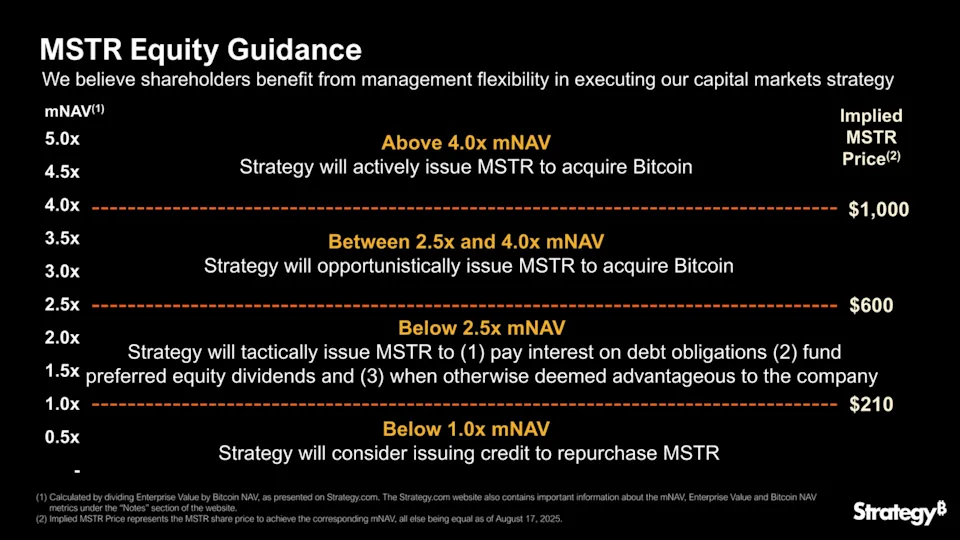

Michael Saylor’s Strategy has become the poster child for corporate Bitcoin treasuries, holding over 713,500 BTC acquired at an average price of roughly $76,000 per coin. With Bitcoin slipping below $75,000 during a broader crypto selloff, the company’s treasury has moved underwater, with unrealised losses estimated between $750 million and $1 billion. The market response has been severe. Strategy’s stock is down 56% over the past year, now trading at a $48 billion market cap, below the estimated $53 billion value of its Bitcoin holdings, pushing its market to net asset value (mNAV) to ~0.90x.

An mNAV below 1.0x signals that public markets value Strategy at less than its underlying assets, weakening the case for equity based Bitcoin exposure versus holding BTC directly. There is no immediate risk of forced liquidation. The BTC is largely unencumbered and the firm recently lifted its preferred dividend to 11.25% to maintain access to capital. However, the leverage embedded in the structure cuts both ways. If Bitcoin remains depressed, Strategy faces higher financing costs, potential dilution, and growing activist pressure to unlock value through buybacks, restructuring, or asset sales (like BTC). In a prolonged downturn, the equity risks becoming a discounted proxy rather than a premium vehicle, damaging the reflexive flywheel that previously drove outperformance.

Similar dynamics are emerging across the broader digital asset treasury (DAT) sector. BitMine Immersion Technologies (BMNR), an Ethereum focused treasury company holding roughly $13.5 billion in digital assets, primarily ETH, has seen its equity sell off alongside peers during the 2026 retracement. Many DATs now trade at mNAV discounts below 1.0x, following heightened volatility and deleveraging events such as October 2025’s 40% drawdown.

Digital Asset Treasuries (DAT) mNav

This signals a structural shift. The DAT premium trade has broken. Where mNAV premiums once enabled reflexive capital raises and balance sheet expansion, persistent discounts now stall funding, amplify volatility, and expose execution risk. For less leveraged players like BitMine and Strategy, forced selling remains unlikely in the near term, but extended drawdowns risk confidence erosion and shareholder pressure for liquidation or strategic alternatives, especially as investors question whether DAT equity adds value beyond direct asset exposure.

For smaller and less established DATs, sustained mNAV discounts introduce an additional risk. They may become acquisition targets. When equity trades materially below the net value of underlying BTC or ETH holdings, even after debt, operating costs, and legal considerations, it can be more attractive for strategic buyers to acquire the company outright rather than accumulate assets in the open market. In effect, discounted DATs can function as indirect vehicles for acquiring Bitcoin or Ethereum below spot, particularly where treasury, regulatory, or public market synergies exist. As a result, weaker DATs may face consolidation rather than recovery, marking a shift from speculative premium expansion to value driven takeovers in the next phase of the cycle.

Hyperliquid Is Turning Volatility Into Revenue

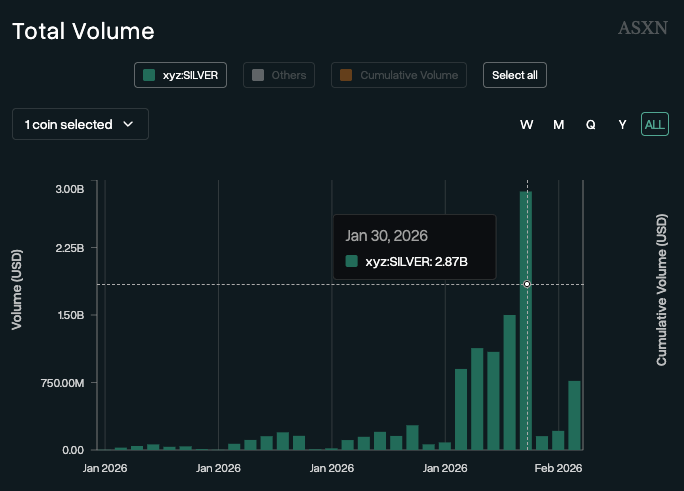

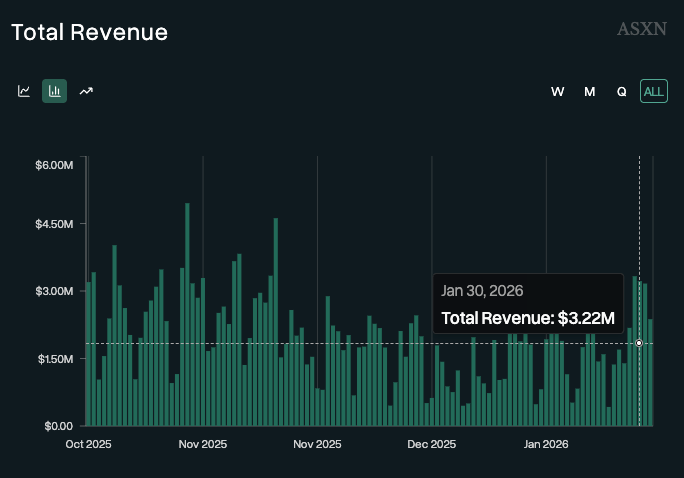

Hyperliquid continues to separate itself as the most dominant revenue venue in crypto, increasingly capturing real market share beyond just perp traders. During January’s precious metals rally and sharp crash, Hyperliquid emerged as a material venue for commodities trading, processing roughly $1–3B in daily silver volume and reaching over $1.7B in total commodities open interest. At peak volatility on January 30, the platform handled ~$3B in daily silver volume, generated $4.5M+ in fees, and held an estimated ~2% market share relative to CME’s primary silver market, a meaningful number.

Importantly, when the crash hit, Hyperliquid absorbed $71M+ in liquidations across ~3,200 accounts without network failure, reinforcing that the platform is built to survive stress events, not just trend environments. That volatility also flowed directly into fundamentals, with the metals unwind helping drive $71.9M in monthly revenue and three consecutive $4M+ revenue days (Jan 29–31), strengthening the buyback flywheel where higher fees mechanically translate into more HYPE accumulation.

On the supply and product side, Hyperliquid delivered another major update this week. The team confirmed that its February unlock has been reduced dramatically, with what was originally expected to be ~9M HYPE (~$300M) entering circulation now cut to just ~140K HYPE (~$4.7M), removing a major near-term supply overhang. At the same time, the protocol unveiled HIP-4, expanding into prediction markets and options, importantly designed without leverage or liquidations, broadening Hyperliquid’s addressable market beyond perp-native activity and pushing it closer to a full-stack on-chain trading venue. The market responded positively, with HYPE jumping ~10% on the announcements.

Independent Reserve Bought out by IG

IG Group’s acquisition of Independent Reserve this week is another Australian crypto brokerage being absorbed by larger global players. The deal valued Independent Reserve at A$178M, with IG taking a 70% stake upfront and the option to acquire the remaining 30% over time. Independent Reserve was founded in 2013 and has been one of the longer-standing Australian exchanges, so the acquisition carries weight beyond just headline value.

It also follows the same consolidation trend we’ve already seen locally, including Caleb & Brown being acquired by Swyftx. While this type of deal reinforces how valuable Australian distribution has become, it also continues the shift toward more institutional, standardised platforms. Historically, when brokerages get acquired, the client experience often becomes less personalised and more “one size fits all,” which tends to create a gap in the market for specialist firms that prioritise service, speed, and broker support.

Australia Shifts Back Into Tightening Mode

Australia’s macro backdrop took a sharp turn yesterday, with the RBA raising interest rates by 25bps, a move that stands out as most developed economies are in easing mode. After cutting three times in 2025, the RBA has now reversed course within six months, making it the first major central bank since Covid to shift from cuts back to hikes. The core issue is persistent inflation pressure, and the RBA is effectively signalling that demand remains too strong, driven in part by elevated government spending, to allow inflation to fall back into target cleanly.

For households, the impact is immediate. A typical ~$700K mortgage now faces roughly an extra ~$105 per month, and markets are already pricing the risk of another hike as early as May. The bigger takeaway is that Australia is now running a very different policy path to the U.S. and Europe, tighter financial conditions locally, even as global liquidity trends improve, which keeps pressure on consumers and raises the bar for risk assets to sustain momentum domestically.

General information only. This article is for educational purposes and does not constitute financial, investment, legal or tax advice, nor a recommendation to buy, sell or hold any asset. Cryptocurrency is a high-risk asset and you should consider your own circumstances and seek independent advice before making any decision. Uptrade does not make price predictions.

Kane leads our international research division, delivering clear, actionable insights into crypto markets and emerging investment opportunities. A true “crypto native,” he has over seven years of hands-on experience, formal qualifications in finance and economics, and has worked across Web3 hedge funds, venture capital, and leading incubators.

View all articles